Greetings from Team Carnelian!

“History doesn’t repeat itself, but it often rhymes.” — Mark Twain

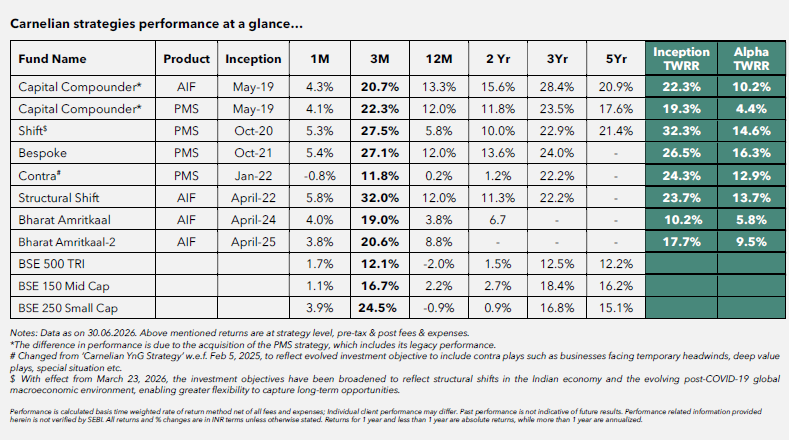

In 2020, Carnelian launched India’s first manufacturing-focused fund – Shift Strategy – at a time when the “India manufacturing” theme was not yet mainstream conversation. More than five years later, the fund delivered 32%+ CAGR, and the thesis that once sat outside consensus is now widely discussed and adopted.

Along the way, we have written about this theme multiple times as the story evolved. In April 2022, “Manufacturing All Stars Aligned” argued that policy push, cost competitiveness, China+1, and India’s 4Ds (Demand, Demographics, Democracy, Domestic markets) had finally created the conditions for a manufacturing renaissance. In May 2024, “Bharat Amritkaal Series India”, Factory to the World updated the thesis with historical parallels to the rise of Japan, Germany, and South Korea. Between these landmark letters, we have also reiterated our conviction whenever the theme was questioned including through the periodic drawdowns when markets rotated away from manufacturing.

It’s now almost six years since we launched – a good time to revisit the thesis honestly.

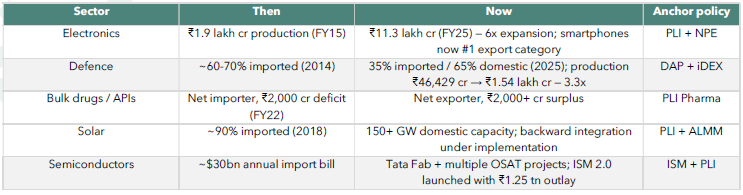

On the positive side, the setup has genuinely progressed. Electronics manufacturing has been the standout – mobile phone production has crossed ~$56 billion, iPhone exports have crossed ~$17 billion, and Apple now assembles 20%+ of its global iPhone volumes here. Tata has committed ~$13 billion to semiconductors. Defence exports have crossed ~$2.5 billion — up from near-zero a decade ago.

However, there is room for improvement to achieve the targeted 25% GDP share from manufacturing. Specific themes have delivered; the macro inflection has not. So why? Global demand headwinds, US tariffs at 50%, the sheer scale of what China already built, and the reality that structural transitions take longer than a single policy cycle to translate into GDP-share shifts.

The fair question then becomes: when does the actual acceleration happen – the one that changes the shape of the economy? We believe it is starting to happen now. And here is specifically why.

Everything we wrote about in 2022 and 2024 – the 4Ds framework, PLI schemes, infrastructure push, and China+1 — remains firmly in place. If anything, the structural base has strengthened, not weakened.

What has changed in the last 18 months, however, is that three powerful accelerants have landed on top of the structural base – simultaneously. This is why we believe the pace is about to shift. Let’s walk through each.

Accelerant 1 – The Currency Reset

The Indian rupee has undergone its most significant real depreciation since 1991. Nominal INR has moved from ~83/USD (early 2024) to the low-to-mid 90s (mid-2026), briefly touching an all-time low of 96.89 in May 2026. But the more important measure is the Real Effective Exchange Rate (REER) – which adjusts nominal INR against a basket of 40 trading partner currencies for inflation differences.

The cumulative REER decline from December 2024 to April 2026 is ~16% – the sharpest sustained real depreciation for Indian manufacturers since the 1991-93 crisis. And here’s the more important observation: in every major Indian REER depreciation of the last three decades, exports have responded.

The current episode is comparable in magnitude to 2013 but has already happened faster (16% in 16 months vs 14% over 3 years). And it is landing on top of the largest manufacturing policy stack India has ever assembled – creating a compounding effect that the 2013 episode did not have.

In plain terms: an Indian manufacturer exporting today has received a ~16% structural cost advantage versus 18 months ago – without changing anything about their cost base. And specifically, against Chinese manufacturers – the relevant competitor in a China+1 world – INR has depreciated ~15% against the yuan in the last year alone. That is the largest single-shot competitiveness reset Indian manufacturers have received in over three decades. And history – our own – tells us what happens next.

Accelerant 2 — The Trade Access Explosion

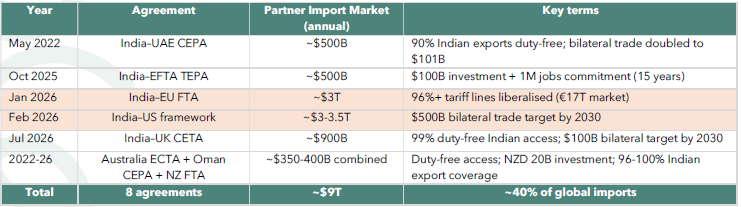

In just four years (2022-2026), India has quietly transformed from being one of the most FTA-cautious major economies to having preferential trade access to ~$9 trillion of global imports — roughly 40% of the world’s total import market. The scale and pace of this shift is genuinely unprecedented in Indian economic history.

But do FTAs actually deliver? The UAE CEPA (in force May 2022) is the clearest proof of concept:

This is what a working FTA looks like: real trade growth, real diversification, real MSME participation.

The India-EU FTA (concluded Jan 2026, expected in force early 2027) is the scale event. 450 million consumers, €17 trillion market, 93% duty-free access for Indian exports. India-EU goods trade is ~$130bn today – well below potential given the size of the relationship.

Combined with the UK CETA (99% duty-free from July 2026), EFTA TEPA ($100bn investment commitment), and the US framework, Indian manufacturers now have equal or preferential access to almost every major consumption market in the world.

Accelerant 3 – The Interaction Effect

Individually, a 10%+ currency reset is good. Individually, an FTA cluster is good. But the real story is that these two forces work multiplicatively, not additively.

Consider a concrete example: an Indian textile manufacturer exporting to Europe.

This stacking is not a marginal shift. It is a China-1994-magnitude reset. It is what allows an Indian manufacturer competing against Vietnamese, Bangladeshi, or Chinese producers to genuinely win – not on quality alone, but on price plus quality. That was the missing ingredient for four years. It has arrived.

The other side of the story: Import Substitution

The manufacturing thesis has a second engine – quieter but equally powerful. Import substitution driven by a 1.4 billion strong domestic market. India still imports ~$775 billion of goods annually. Every rupee of that import bill replaced by domestic production is direct manufacturing GDP – with no dependence on global demand or export competitiveness. The playbook is already delivering – hard numbers, not projections:

The currency depreciation makes this second engine even more powerful. Imports become more expensive; domestic manufacturers gain natural pricing power. This is exactly what China exploited from 1994 onwards – a devalued currency doesn’t just help exporters, it also protects domestic producers from imports.

The export accelerants get the headlines. The import substitution engine works quietly — and for 1.4 billion consumers, it may be the larger opportunity over the next decade.

What history says – China 1994 and the Pattern of Manufacturing Miracles

Every manufacturing miracle in modern economic history has been preceded by a version of the same stack: sustained currency reset + expanded trade access + policy support + massive infrastructure capex. Japan post-1949 (yen peg at ¥360/USD for 22years), South Korea post-1961, Vietnam post-2007. But the cleanest parallel for India today is China from 1994 to 2014.

On January 1, 1994, China unified its dual exchange rate system, devaluing the yuan by 33% in a single move. China then fixed the yuan at 8.3 RMB/USD and held that peg for 11 years. In December 2001, China acceded to the WTO – gaining preferential trade access to essentially the entire developed world in one stroke. What happened next is the closest thing to a modern economic miracle:

The currency depreciation alone was already helping exports. But look at the power of the interaction effect once WTO access arrived – exports grew 10x in 2001-14 versus ~2x in 1994-2001. The academic evidence (Erten and Leight, Review of Economics and Statistics, 2021) confirms the mechanism: WTO accession reduced trade policy uncertainty and triggered a large reallocation of labour and capital from agriculture into manufacturing.

The Vietnam parallel is instructive. For the past decade, when the world talked about China+1, Vietnam has been the biggest gainer. Since joining the WTO in 2007, Vietnam’s exports grew from $48 billion to over $370 billion – nearly 8x in 16 years, versus ~3x for India over the same period. Samsung makes more phones in Vietnam than in South Korea.

But Vietnam is now reaching a tipping point. Labour costs have doubled since 2010. Trump’s tariffs signal its “neutral third country” status is eroding. And with only 100 million people, its scale advantages are running out. India – with its structural case, its accelerants, and its 1.4 billion consumers – is now best placed to capture the next phase of manufacturing and exports growth.

What could go wrong now?

These are real. None of them changes the direction of the thesis – but they could affect the pace.

A major overhang has eased now

Through much of early 2026, oil was one of the biggest overhangs on India’s macro story – the Gulf conflict took Brent above $120 and put simultaneous pressure on fiscal, CAD, INR, and inflation. With oil moderating, and the geopolitical situation stabilizing, that overhang is easing. Public capex in the Union Budget 2026-27 was raised to a record ₹12.2 lakh crore – 4x a decade ago – and every $10/bbl fall in oil frees up ~$14-15 billion of annual import bill for the government to redirect toward PLI extensions, industrial parks, and infrastructure completion.

Where we see the opportunities

The macro setup translates into concrete portfolio opportunities. Some manufacturing pockets stand out.

Second-order beneficiaries: financials (bank credit expansion typically accompanies every manufacturing boom), consumption, and premiumisation – as rising manufacturing wages compound into discretionary spend.

Our portfolio is positioned overweight across these themes.

Conclusion

Every economy that has made the transition from services-led or agricultural to a manufacturing powerhouse – Japan, Germany, South Korea, China, Vietnam – has done so on the back of the same stack of accelerants: sustained currency reset + expanded trade access + policy support + massive infrastructure capex + decisive leadership.

India has now, for the first time in its history, all five elements aligned simultaneously. The structural case (which we wrote about in 2022 and 2024) is intact. The cyclical accelerants (which we’re writing about today) have arrived. The near-term risks are easing.

This is the moment we have been waiting for since we started writing on manufacturing in 2020. The stars are not just aligned – the accelerants have arrived.

But being right about the theme is only half the battle. India’s IT boom created wealth for names like TCS and Infosys – and destroyed it for those who chased second-line names at any price. The theme is necessary, but it’s not the only thing.

Stock selection, business quality, management pedigree, and valuation discipline are what separate wealth creation from theme participation. We remain super bullish on manufacturing in India — but equally disciplined about how we participate. Stay disciplined. Stay invested.