Greetings from Team Carnelian!

“The four most dangerous words in investing are: this time it’s different.” — Sir John Templeton

In 2021, we wrote “FAD — FOMO — FADE”, warning about the new-age tech IPO frenzy. In 2025, Part 2 cautioned against the unlisted shares and preferential allotment bubble. Both times, the framework helped our investors sidestep significant losses. This is the third letter in the series. The setting is global this time. But the script, as you will see, is identical.

Markets repeat the same cycle. Only the cast changes.

FAD is the narrative phase, a theme becomes “the next big thing,” the early winners get amplified everywhere, and valuations stretch well beyond fundamentals. FOMO sets in when the fear of watching others get rich overrides the discipline of knowing what you own. And then comes FADE. Reality reasserts itself. Valuations correct. Losses crystallise. And everyone asks how they missed it even though, in hindsight, every sign was there in plain sight.

Each cycle arrived with its own story and its own “new metrics.” Each one felt different while it was happening. And each one ended the same way.

Today’s FAD: the global AI frenzy

In almost every client conversation over the last few months, the question has been some version of: “How are you playing AI”, “How do I get into the AI trade?” or “Can I buy OpenAI or SpaceX through GIFT City?” It is the same conversation we heard in 2021 and 2025 just with different names. And as always, the tell is in sequence: when the first question is about access rather than analysis, when the price comes up before the business, we have been here before.

Consider what is queuing up. Three of the most anticipated IPOs in modern financial history are arriving almost at once SpaceX targeting a $1.75 trillion valuation, OpenAI last raised at $852 billion, and Anthropic at $965 billion. Together, roughly $4 trillion of new market value, about the size of the entire Indian stock market, set to hit public markets in a single window. History is unusually consistent on what this kind of clustering means. In 1999–2000, UPS and AT&T Wireless listed at the dotcom peak; the Nasdaq then fell 78% and took 15 years to recover. In 2007, Blackstone’s IPO marked the top of the privateequity cycle; the S&P 500 fell 57%. In 2021, Coinbase, Rivian, and Robinhood all listed near the peak of their manias; each fell 70–95%. The IPO never causes the top, it is enabled by the very euphoria that creates it. That all three of these companies are loss-making today is a footnote almost no one is pausing to read.

What the euphoria looks like on the ground

To see how far this has travelled, look at South Korea. Retail investors there are surrendering life insurance policies, breaking fixed deposits, and taking margin loans to buy Samsung and SK Hynix. Insurance surrenders at the three largest life insurers jumped 16% in Q1 2026; margin debt to buy semiconductor stocks in Korea have been quadrupled to ₩8 trillion in months; and the country’s margin-loan balance rose 72.5% in a year against 36% in the US and 5% in Taiwan. The detail that stays with you is who is doing it: investors in their sixties are among the largest participants, leveraging a lifetime’s savings into a single chip trade at record prices. And on 27 May 2026, Korea launched 2x leveraged ETFs on these very stocks. When the last product created is a leveraged retail bet on the hottest names, you are not early. You are late.

What almost no one chasing these chips will say out loud, is that SK Hynix’s margins look extraordinary only if you forget the last cycle. They were 52% in 2018, collapsed to -24% in 2023, and are back at 72% today riding entirely on AI memory chips, where every dollar of profit traces to hyperscaler spending from Nvidia, Google, Microsoft, and Meta. The moment that spending merely pauses, prices fall and margins revert. We saw it in 2019. We saw it again in 2023. The man in Seoul cashing out his insurance policy is betting the memory cycle has been abolished. It never has.

AI is real. The price is not.

Let us be clear, because this is the heart of the matter. AI is one of the most transformative technologies in human history. We believe that without reservation. The productivity gains are real, enterprise adoption is accelerating, and what AI does over the next twenty-five years will very likely exceed almost anything we can picture today.

Sir John Templeton warned that the four most dangerous words in investing are “this time it’s different.” The irony is that the believers are usually right about technology and extremely wrong about price. In March 2000, Cisco was the picks and shovels of the internet: real revenue, real earnings, 55% growth, a genuine moat. Over the next 25 years internet usage rose 14-fold, Cisco’s revenue tripled and its earnings quintupled and the stock returned all of 0.2%. Closer to home, Wipro’s 2000 peak took twenty years simply to reclaim. In both cases investors were entirely right about technology. They merely paid the wrong price. Cisco at the dot-com peak traded at 31x revenue. SpaceX is asking for 93x, OpenAI 35x, Anthropic 21x and all three are still loss making.

The futurist Roy Amara captured this better than anyone: we overestimate what technology will do in the short run and underestimate what it will do in the long run. That is exactly the trap today. In the short run, the market is pricing AI as if every promise has already been delivered, as if the $200 billion now being poured into data centers is already producing the recurring profits these valuations demand. It is not. In the long run, AI will almost certainly do more than even today’s bulls imagine but the companies that capture most of that value may not even be public yet and are unlikely to be the ones whose IPO you are being offered today at 93x sales. “The technology will be transformative” and “the entry price today is sensible” are two entirely different statements. Mistaking one for the other is among the oldest and most expensive errors in investing.

The fingerprints of a top

Every genuine bubble leaves the same fingerprints, in concentration, in valuation, and in leverage. Today they are everywhere you look.

What looks like “global diversification” is really one bet. Samsung and SK Hynix together touched 42.2% of Korea’s KOSPI in May 2026, briefly crossing half the index. TSMC alone is over 40% of Taiwan’s market. The Magnificent 7 are about 34.5% of the entire S&P 500 against the largest single stock, GE, at just ~4% in 2000. A portfolio spread across the US, Taiwan, and Korea today is not diversified at all. It is the same concentrated bet on the AI hardware chain, wearing three different index labels and a single slowdown in data center spending would hit all three at once.

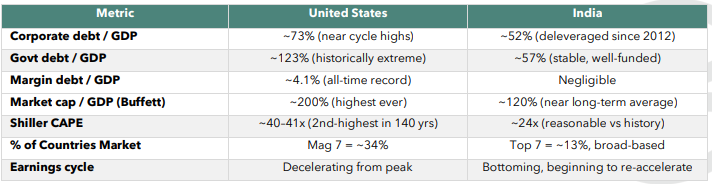

US valuations have rarely, if ever, been here. America now makes up over half of global equity market value, a first in recorded history and more than 60% of the MSCI All-Country World Index, up from around 30% in 2007. The Buffett Indicator, market value to GDP, sits near 200%, the highest ever recorded, above even 1999. The Shiller CAPE, which smooths earnings over a decade, stands at roughly 40–41x, the second-highest reading in 140 years, behind only December 1999. Buying US equities at a CAPE above 40 has historically delivered close to zero real return over the following decade. Not a crash; just ten

years of going nowhere.

And strip out AI, and the growth simply is not there. For the full year 2025, Magnificent 7 grew their earnings by roughly 22%. The other 493 companies in the S&P 500, the banks, retailers, manufacturers, healthcare firms, the real economy grew by about 9%, less than half the pace and it gets narrower still. For 2026, analysts expect the Magnificent 7 to grow earnings ~23% again but strip out a single stock, Nvidia, and that figure more than halves to ~13%. For the first quarter of 2026, Mag 7 earnings growth without Nvidia collapses from 23% to just 6%. The engine of the great American bull market is not seven companies. On closer inspection, it is increasingly one that Nvidia keeps ~80% of the AI chip market, at extraordinary margins, more or less forever the very company whose market share a Microsoft backed challenger began contesting this week.

They are no longer building businesses. They are building stock prices.

Watch where the incentives now point. Meta has filed documents tying senior executive pay to a $9 trillion valuation by 2031, a 500% rise from today’s $1.5 trillion. Tesla shareholders approved a roughly $1 trillion package for Elon Musk tied to an $8.5 trillion market-cap target, for a company that just posted its first-ever annual revenue decline, with net income down 47% to $3.8 billion and the stock at 327x earnings. Musk’s award requires 20 million vehicles a year, a million robotaxis, and a million humanoid robots; Tesla delivered 1.8 million cars last year. Meanwhile Meta’s stock-based compensation consumed 96% of its free cash flow, $42 billion not returned to shareholders but spent betting on its own share price.

The playbook never changes. Make extraordinary promises about the future. Tie pay to the stock price rather than the business. Spend billions on unproven bets. Use the promise of transformation to justify a price with no relationship to present reality. Technology changes, the pitch changes the ending does not. Stock prices follow earnings. Always have. Always will.

Now stand India next to all of this

Here is why this matters so much for us. Every stress we have just described, leverage, valuation, household fragility, concentration reads the opposite way in India. The same lens that flags danger abroad flags opportunity at home.

India is not merely cheaper. It sits on the other side of nearly every metric that defines risk in this cycle less levered, less concentrated, more reasonably valued, with an earnings cycle turning up rather than rolling over.

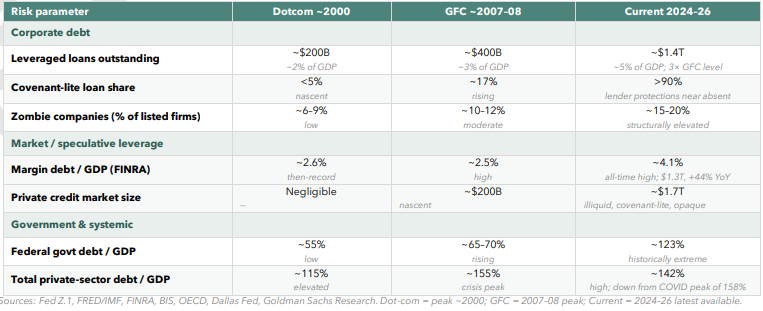

And this time, the ground beneath the market is weaker than in either crash before it.

Each of the last two great unwinding had a single fault line. The dot-com bust was an equity event — corporate and household debt were modest, and the government had room to respond. The 2008 crisis was a housing and household-debt event, transmitted through the banks. What makes today different, and more fragile, is that for the first time every fault line is stretched at once — and the cushions that absorbed the last two shocks are far thinner.

Read the last two rows together. “Covenant-lite” lending loans with almost no protection for the lender has gone from under 5% of the market to over 90%, while a $1.7 trillion private-credit market that barely existed in 2008 now sits largely unregulated and untested. And unlike 2000 or 2008, neither the government nor corporate America has the balance-sheet room to ride to the rescue. That is why a fall, when it comes, will likely take far longer to recover from in the West and that is why where you are

standing when it hits matters more than ever.

Why the flows have temporarily left — and why they return

If India is in such good shape, why has it lagged? The MSCI Emerging Markets index tells the story in numbers. Three years ago India was the second-largest weight in the index at 21%. Today it slipped to fourth at 11.9%, while Taiwan has climbed from third to first at 24.8% and Korea from fourth to third at 18.7%. India’s weight did not fall because its fundamentals weakened, its economy has grown faster than both Taiwan and Korea over this period. It fell because passive global capital mechanically chased the AI hardware trade through TSMC and SK Hynix, lifting their index weights and mechanically reducing everyone else’s.

In other words, every global index fund bought over the last two years has been quietly underweighting the world’s fastest growing large economy while overweighting two markets concentrated almost entirely in a single cyclical chip trade. When that trade cools and index weights rebalance, the country that lost weight through no fault of its own but only through someone else’s rally, becomes the natural home for returning flows. That country is India.

India will not be spared the fall — but it is built to recover. We owe you one honest caveat. If the global AI trade unwinds in a sharp, vertical fall, India will go down with everything else in the first leg. When the dot-com bubble burst, even high-quality Indian companies fell 40–60%. When Lehman failed, India corrected 60% despite being fundamentally unscathed. In a true global risk-off, correlations go to one and capital exits everywhere at once. But what happens next is where the fundamentals decide the outcome. Markets standing on excess leverage, broken zombie balance sheets, take years and sometimes decades to climb back. A market standing on low leverage, healthy households, reasonable valuations, and a rising earnings cycle does not. India falls with the tide, but it rises first and rises strongest, because the foundation underneath it is genuinely stronger. That is the whole point.

So, what should we actually do?

Separate the technology from the price. The question is never “Is Open AI a great company?” it almost certainly is. The question is: “Am I buying Open AI at 35x revenue, the way investors bought Cisco at 31x in March 2000 and then waited twentyfive years to break even?”

Do not act out of FOMO. Three mega-IPOs arriving together is not the start of the AI trade. It is the market monetising the narrative at maximum valuation which historically means we are closer to the peak of euphoria than its beginning.

Avoid distraction. One badly timed bet, sized wrong, can erase a decade of patient compounding. As we have always said: surgery must be done by surgeons.

Closing thought

In 2021 we warned about new-age tech listings; that FAD faded. In 2025 we warned about unlisted shares and preferential allotments; we know how investors lost money. Today the cycle is global, the names are larger, the narrative is louder, and the sums involved are bigger than anything we have seen in a generation. But the playbook is identical: extraordinary promises, pay tied to share prices rather than profits, leverage at generational highs, concentration at unprecedented levels, and valuations that demand a future no one can guarantee on a timeline no one can know.

AI will be transformative; we are almost certainly underestimating what it does over the long run. But by the same logic, the market is wildly overestimating what it can deliver in the short run, at these prices. The two halves of that truth are inseparable; you cannot honestly hold one without respecting the other.

We do not need to call the top but recognize that we are in a very late cycle. If this bubble burst, India will not be spared. To our mind, AI is the biggest risk to global markets (including India) today.