We started the year by writing to you that we expect this year to be volatile and a year of de rating (link). We are already witnessing the same though, we must admit that we didn’t expect this kind of a disorderly & sharp fall.

Markets don’t like surprises, especially negative ones. The Ukraine war and China lockdown created a huge impact on the energy prices, food prices and commodity prices along with the continued disruption in the supply chain. This further compounded the problem. While inflation was expected, but all these factors created a sudden spike in inflation which forced most central banks to react firmly and decisively prompting a sharp rise in interest rates (e.g. Fed raising 150 bps in just 4 months – not seen in the last 40 years!). The markets turned from a complacent world to a one full of worries in just a few months. This led to a huge wealth destruction across the globe specially where capital was available freely such as New Tech, Crypto, etc. and in fixed income markets.

As we stand today, one thing is very clear that the inflationary expectations are high. However, it also seems reasonable to assume that from the recent sharp drop in commodity prices, inflation might have peaked out. Of course, now the narrative has shifted or is shifting to “Growth”. What is the implication of slow growth or a possible recession?

Markets are full of worries and uncertainties and investors are seeking what to do from here. A few questions which everyone is seeking answer for are:

– Is the US going into recession?

– Implication on India of a slow growth / recession in the US?

– Is the India story intact? If yes, is it going to see more sell off or has it bottomed out?

– How long will the FII sell flow continue?

We are sharing our views on these questions through this letter:

Is US into recession?

There is no doubt that high inflation & interest rates will lead to slowdown in demand and economy. Whether it will go into recession – only time will tell and depends a lot on Fed’s QE withdrawal pace, rate cycle and other geopolitical developments. If the Ukraine war stops and energy prices cools off in next 30-60 days, the Fed will breathe easy and can turn soft on withdrawal of liquidity and interest rate cycle. However, if it prolongs for extended period, we think the odds of a recession rise significantly.

What is the implication on India of a slow growth / recession in the US?

US provides huge business to the world, especially to EMs like China. If consumption in the US slows down, it will surely have a related impact on exports of countries supplying to it.

How does it impact India?

– India’s IT exports are largely to developed markets like the US and can have an impact on the growth rate. Although some amount of spend is inevitable as technology which is the backbone and essence of businesses. Technology is also a cost deflator which is the key need in recessionary times. However, one can’t rule out the contraction of demand in the medium run.

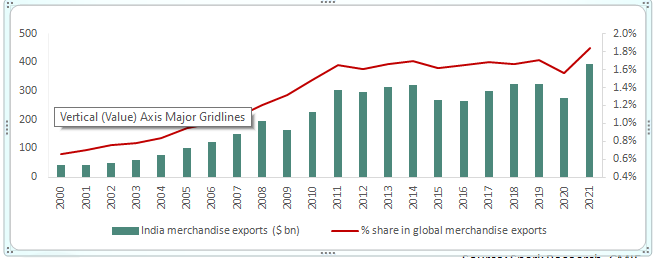

– India’s exports of goods, though a very small proportion of US demand, can get impacted in normal times of slowdown. However, due to China +1 and supply chain diversification, it is unlikely to slow down this time. What India loses due to a growth slow down, can be gained through a market share increase. However, some quarters of disruption in earning is always a possibility.

Slow down can lead to a drop in the commodity prices, which is positive for India in the medium term.

In essence, there could be an impact on the Indian economy for a few quarters which could even impact earnings, but it would not structurally de-stabilize the India story.

Is the India story intact? If yes, is it going to see more sell off or has it bottomed out?

India’s story is of domestic consumption, acceleration in investment cycle, a pick up in credit offtake and pick up in Indian exports. None of these are under threat. In fact, all three D’s (Debt, Demography and Deregulations) are in favour of India to propel and keep its economy growing the fastest in the world on a structural basis.

Of course, we must embrace a slowdown in earnings in the short term. During such uncertain times, businesses are facing a lot of challenges which naturally reduces the focus from growth to risk management. We think we will see slowdown in the earnings growth for the FY 23. Downgrades are more likely to happen and that could lead to some corrections. While a lot of it has been factored in the market but one can’t rule out some more downside as we progress through the year.

Considering FY23 earnings at 17% growth and historical average of 13% CAGR over the last 20 years, the Nifty is trading at a 1 year forward PE of 17.5x (in-line with its broader range of ~ 16x-19x). (Source: MOSL, Bloomberg)

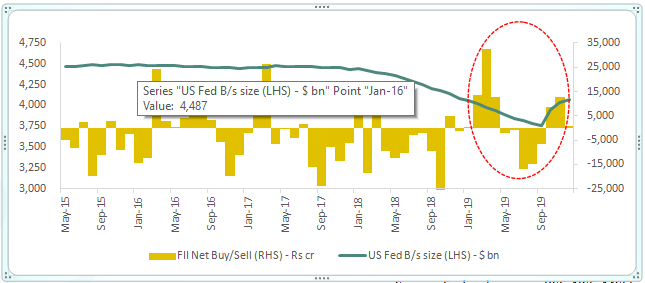

How long will the FII sell flow continue?

One of the most common question and worry is the continued sell flow by FIIs. How long it can continue? If we look at historical patterns, foreign portfolio flows typically turn negative towards EMs including India when Fed starts talking about tightening or raising rates.

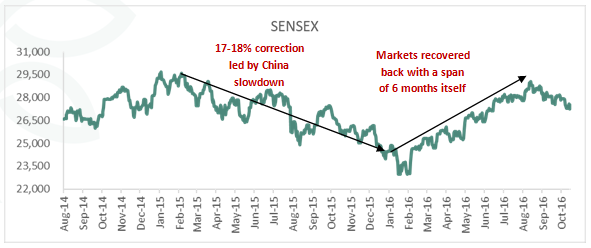

In 2015, in anticipation of fed raising rates, FIIs withdrew INR 37,000cr in 2H of CY 2015 from the Indian equity markets vs a buying of INR 87,000cr in CY 2013 and INR 67,000cr in CY 2014.

We think with the interest rates peaking out and the pressure easing off through rest of 2022, it should ebb and 2023 should be a positive year. This was reflected again in 2019 when fed backed off from tapering and flows turned positive – buying INR 40,000cr in CY 2019.

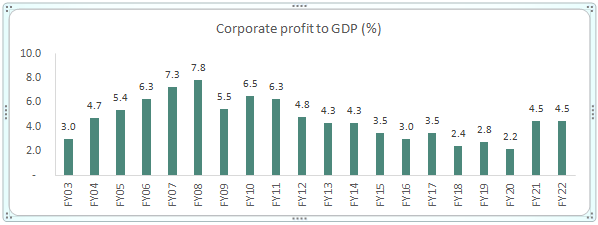

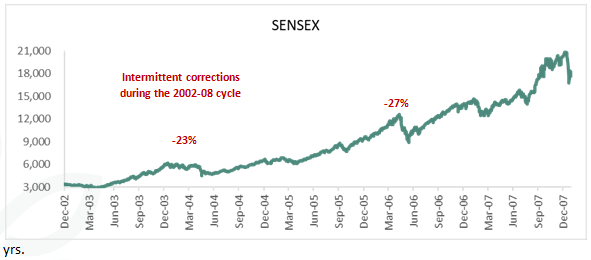

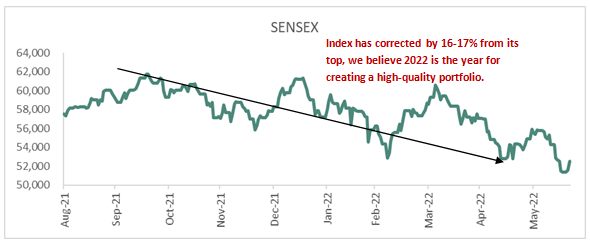

2022 to be the year of portfolio construction Over the last 9 months, Nifty has corrected by 16-17% from its top. During the 2002-2008 bull run as well, market saw 3 intermittent corrections to the tune of 20-25% each from its respective top. India is in a sweet spot and continues to remain resilient. Our interactions with top-notch corporates indicate that India’s appeal as a global manufacturing hub has continued to improve. Corporate profit to GDP has inched up from the lows of 2.2% in 2020 to 4.5% in 2022. The same was at 7.8% during its peak in 2008. Nifty profits (ex-financials) have grown by 16% in FY21 and 37% in FY22. The same is expected to grow by 17% in FY23 and 14% in FY24. (Source: MOSL, Bloomberg)

Historically, we have seen markets rebounding sharply after each correction as evidenced in below examples. We advise investors to expand their view and look beyond 2022. We believe this is the year where investors should focus on the construction of a high-quality portfolio – which can be the flag bearer over the next 3/5

We know from experience it is the uncertain times which always lead to the road of handsome returns.

Vintage plays an important role in outcome of returns. Next 3-6 months of uncertainty should be used as an opportunity to invest and build this vintage in your portfolio.

We remain bullish on BFSI, manufacturing, automobiles, capex-oriented plays for next 12- 18 months. On a lighter note, we would like to end with a modified version of Kabir’ Doha:

तेजी मे इन्वेस्ट सब करें

मंदी में करें न कोय

जो मंदी में इनवेस्ट करें

सदा मुनाफा होय।

मीडिया सुन सुन के मुआ

पंडित भया ना कोय

सब्र और समझ से काम लें

वही खिलाड़ी होय।

बॉटम बॉटम सब कहे

बॉटम चुना न कोय

जब असल में बॉटम आये

रोकड़ा बचा न होय।