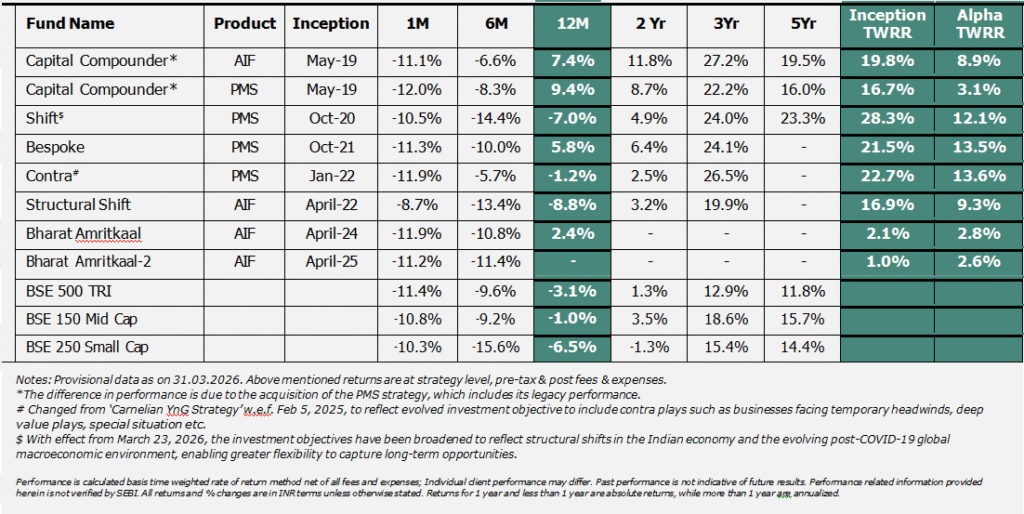

Greetings from Team Carnelian!

Imagine receiving this letter in August 1990, or September 2001, or March 2003, or Sep 2008, March 2020, or Feb 2022. In each of those moments, the headlines were alarming, and the case for unnerving investors felt overwhelming. Every time, there was a compelling narrative for why this time was different—why the disruption posed a uniquely severe risk.

And here we are again, in March 2026, facing yet another crisis: a war triggering major supply chain disruptions, crude above $100, the rupee at 92, India’s 10-year yield crossing 7%, and the Nifty down 11% in a month.

It isn’t different.

What we can tell you—with the full weight of market history behind us, is that in every one of these episodes, without exception, two things have held true: crises end, and earnings endure.

With the benefit of hindsight, each crisis has also created new opportunities.

Let us look at how markets have recovered in the aftermath of past crises:

| Crisis | S&P 500 / Dow Jones (United States) | Nifty 50 / Sensex (India) | ||||

| Peak Decline | Recovery Time | 12M Return | Peak Decline | Recovery Time | 12M Return | |

| WWII — Pearl Harbour (1941) | Dow -17.5% (~4 months) | ~1 year | +50% by war’s end | N/A — Nifty not yet in existence | N/A | N/A |

| Gulf War — Iraq invades Kuwait (1990) | S&P -16.9% (Aug–Oct 1990) | ~4 months | +12% | Sensex -18% (Oct 1990 onwards) | ~4–5 months | +20% |

| 9/11 Attacks (2001) | S&P -11.6% (within 1 week) | 15 days | +15% | Nifty 50 ~- 20% (dot-com bear); Nifty 500 -43% full episode | ~3–6 months | +22% from 2001 lows |

| Iraq War (2003) | S&P -5.3% (~7 trading days) | 16 trading days | +26.7% | Nifty ~-5% (pre-war uncertainty) | ~2 weeks | +82% from 2003 bottom |

| Brexit Referendum (2016) | S&P -3.6% (2 days post-vote) | < 2 weeks | +14% | Nifty -2.5% (June 24, 2016) | ~5–7 days | +18% (FY2016-17) |

| COVID-19 (2020) | S&P -34% (Feb 19 – Mar 23, 2020) | ~5 months | +50% over 1 year | Nifty -40% in 46 days (Jan– Mar 2020) | 7 months | Tripled in 3 years from lows |

| Russia–Ukraine War (2022) | S&P -7% at onset; -19.4% full yr 2022 | ~1 month (onset shock) | ~+15% from onset low; – 19.4% calendar yr | Nifty -7.4% at onset; +4% full yr 2022 | ~9 months (full yr positive) | +4% calendar year 2022 |

| † Sensex proxy used for pre-1996 periods (Nifty 50 launched April 1996). All 12-month returns approximate from peak decline unless noted. N/A = data not available. | ||||||

Why does this happen?

Because war ends and things get normal. Markets recover and the reason comes down to a single concept.

Terminal Value. Let us understand. When you buy a share of any company, you are not buying next quarter’s earnings. You are buying a claim on every rupee that business will ever earn, across its entire lifetime, discounted back to today. In a standard DCF framework, for a well-run company compounding at a healthy rate, ~70–80% of intrinsic value is accounted for by earnings beyond Year 5 with the largest single block sitting beyond Year 10, Terminal value, and it is the dominant driver of what a stock is worth.

While short-term events like this war disrupts one or two quarter of earnings, does not change the terminal value of the business (unless the event is fatal to a business, which can happen to a business but unlikely to happen collectively to all businesses). The decades of compounding that follow, the structural earnings power of the business remains entirely intact. (Just the aside, any investor must constantly monitor and evaluate any permanent change in moat or structural earning power irrespective of an event). So, in case of an event, what changes is sentiment, which is violent, visible, and temporary. What does not change is the compounding engine underneath, which is silent, persistent, and permanent. Markets, in moments of fear, price the sentiment. Patient investors own the terminal value. History is unambiguous on which one wins. The table above beautifully illustrates this.

Let’s understand in the context of a stock.

Let’s take a case of IndiGo. The stock is down 20% since the start of the war due Gulf airspace disruptions, ATF prices surging, near-term profitability under pressure etc. The market’s concern is not irrational. One or two quarters of earnings will be impaired, and we acknowledge that plainly. But here is the question to ask, what fraction of IndiGo’s intrinsic value depends on those quarters? For a franchise with 64% domestic market share and the structural tailwind of India adding 200–300 million air travelers this decade, standard DCF analysis suggests that approximately 85–90% of its value sits beyond Year 10. Terminal value — the earnings this business will generate long after this war is a footnote in a history book — is what you own when you own this stock. Two disrupted quarters represent perhaps 2–3% of that lifetime value. The market has marked it down 20%. After COVID-19, when IndiGo’s stock fell 60%, it tripled within two years. Not because the pandemic was short. Because the flights were grounded, but the business was not.

What this moment calls for is a return to first principles: in the long run, stock returns are determined by earnings throughout the life of the company. Wars, tariffs, FII flows, currency moves — all create violent, alarming noise in the short term. But they are not the signal. The signal is the long-run earnings power of the businesses you own. The only thing that can permanently impair equity returns is permanent impairment to that earnings power and growth. And that is precisely what geopolitical events, with remarkable historical consistency, do not produce. If they produce for some businesses, one should avoid them, but not market.

“Stocks don’t read the newspaper or swoon in response to scary headlines. When they’re priced for desperation, they can rally in the face of desperation.”– The Davis Dynasty

We wrote in our January letter that 2026 is year of opportunity based on a solid recovery we were witnessing in India economy and corporate earnings. In Q3FY26 — the December 2025 quarter — Nifty Small Cap 100 grew net profits 25% year-on- year, their strongest quarter in recent memory. Nifty Midcap 100 delivered 16% profit growth. Even the Nifty 50 EPS came in at +13.4% against a consensus estimate of 10.1% — a meaningful beat at the very top of the market cap spectrum.

| Segment | Q3FY26 Net Profit Growth (YoY) | What It Tells Us |

| Nifty 50 EPS | +13.4% | Beat consensus 10.1% and pace accelerating |

| Mid-Cap (Nifty MC 150) | +16% | Broad-based, not concentrated in 2-3 names |

| Small-Cap Universe | +22% | Strongest quarter in recent memory |

| EPS Upgrades | 36% of companies upgraded | Auto, BFSI, FMCG, pharma leading revisions |

What does this event change:

- This is a significant development in global geopolitical landscape. This will surely redefine future outcome depending on how long it lasts, what are the eventual outcomes.

- The equation between US-Europe.

- US-middle east is unlikely to remain same.

- China seems to be the biggest beneficiary of current crisis who is quietly watching and smiling. Their political and economic ability to endure this pain is quite high.

- India’s energy dependence and vulnerability remain high. While government is trying to manage but India’s ability to endure this pain is surely far lesser than China.

Widened Current Account Deficit due to confluence high oil price, high chip prices and high Gold price (least appreciated cause)

- India’s energy bill meaningfully goes up from USD 90-100 bn to 140-150 bn due to current surge.

- Chip prices have been on rise for last 6-12 months from 40%-250% depending on type of chip. India spends USD 80-90 bn on chips. This is expected to go to USD 130-140 bn in the current year

- India imports average 750 MT of Gold every year. Gold price going up will India’s outgo from USD 50 bn to 80-100 bn.

With this war pushing Oil prices, it has put lot of pressure on India’s already stretched current account deficit, leading to sharp fall in currency. It’s unlikely to repair in a hurry and India needs to take concrete steps to repair it on a war footing basis.

What this event doesn’t change:

- Structural drivers in place

- Corporate India has the strongest corporate balance sheets in a generation,

- a pro-growth policy environment both from fiscal and monetary policy.

- India’s demographics

- India’s low inflation base

- Strong Banking system

- India’s strong fiscal situation

Our view & guidance

There is no permanent impairment to the terminal value of the India story. This event will, of course, create short-term disruptions—likely denting earnings for a couple of quarters, or longer depending on how the war evolves.

But this is not new. India has navigated crises before—1991, 9/11, the 2008 GFC, Brexit, demonetization, COVID-19, and the Russia–Ukraine conflict. Each time, the headlines screamed permanence; the underlying data suggested continuity. And each time, investors who focused on the data emerged stronger.

Experience also tells us that markets bottom well before the crisis itself ends. During COVID-19, markets bottomed on the day of the lockdown. During the Ukraine conflict, markets bottomed in June—well before the situation stabilized. More recently, markets turned ahead of the resolution of tariff concerns. The pattern is consistent.

Every crisis brings opportunity. With the evolving US–Europe equation and India’s FTA with Europe, businesses with a strong European focus could see meaningful tailwinds. We are actively looking for such opportunities. While we cannot control external events, we can adapt—reallocating capital where we see better or emerging opportunities.

There is a certain kind of investor who does extraordinarily well overtime. They are not necessarily smarter or better informed. What they possess is a rare, almost stubborn conviction: that the businesses they own will be worth more in the long term than they are today—and that the headlines in between are largely noise.

We remain committed to that philosophy—continuously reassessing our portfolio to ensure we own high-quality businesses with enduring value. Crises create vintages. As history shows, these periods often offer the foundations for future returns.

Build this vintage.